The statistics aren’t pretty. 60% of restaurants don’t make it past their first year and 80% go out of business within five years. Despite the hurdles, many restaurant owners and operators believe that as long as they’re making money, they’re doing “good enough.” The failure in this approach is that it doesn’t account for a universal truth—costs increase.

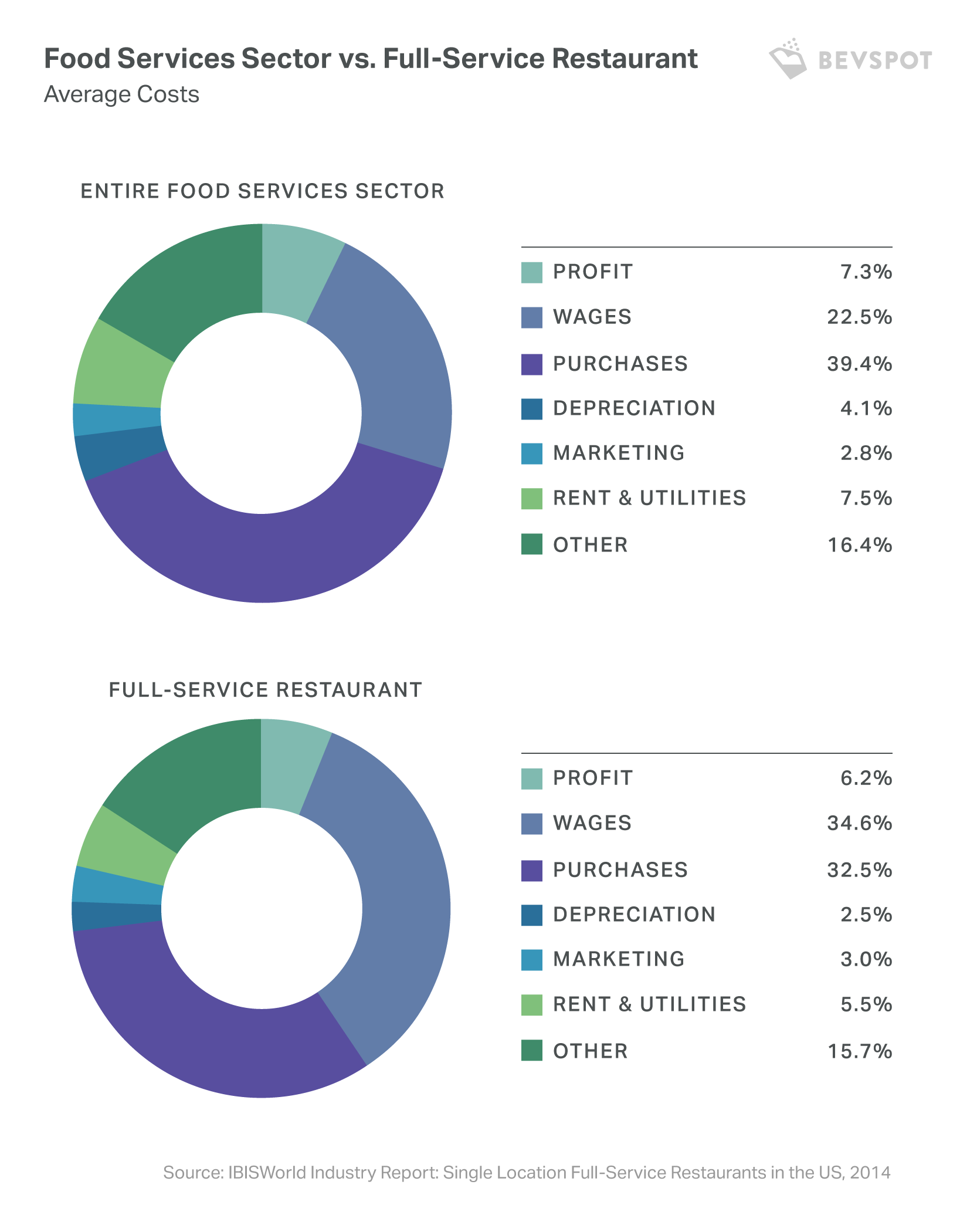

According to a 2014 IBISWorld report on single location full-service restaurants in the U.S., 67% of a restaurant’s costs go directly to wages and purchase expenses. Additionally, the average profit margin for a restaurant, after removing all other costs, is only 6.2%. With a profit margin this slim, insolvency is unfortunately never far away.

The biggest risk for the restaurant industry is rising wages and increasing food costs. If you’re not constantly working to improve profitability and grow your revenue, the costs will take over. It’s imperative that you’re consistently and actively reducing costs to maintain your current level of success. How can you do this? Improving efficiencies.

Competition in the restaurant industry is at a recent high. In 2016, restaurant location growth reached 1-1.5%, a level we haven’t seen since the early 2000’s. The catalyst of this growth? According to the Jefferies Restaurant 2016 report, independent and chef-driven concepts are adding to the supply in a crowded market.

It’s classic supply and demand economics—the greater the supply, the lower the prices. Competition amongst restaurants in the United States is both driving down menu prices and making it more difficult to increase them. And it’s not just competition from similar concepts. Limited service restaurants (including quick service and fast casual) are one of the fastest growing segments in the food service industry. Sales at these restaurants grew from $160B in 2009 to a forecasted $234B in 2017. The rise in low-cost limited service restaurant sales adds additional pricing pressure on traditional full-service restaurants competing for the same customer.

Wages represent a significant portion of your operating costs—34.6% according to IBISWorld—and you can expect that number to increase for a few reasons:

Thanks to the high turnover rate and a record low unemployment rate, it’s becoming harder and harder for restaurant owners to keep people without increasing payroll. If your restaurant is in one of the 18 states with new minimum wage laws, you may already be experiencing the crunch. All of these factors create incredible opportunities for those looking to work in the restaurant industry, but it’s not so great for your bottom line.

32.5% of your restaurants’ costs go towards purchasing the actual food and beverages. We all know how much these costs can fluctuate and how challenging it is to pass the difference on to the customers. Since August 2016, the food producer price index (PPI)—the change in food costs—accelerated by 7.7% according to the February 2018 Credit Suisse Equity Research Restaurant report. In addition, increasing consumer demand for healthier, organic, and local ingredients is putting greater pressure on restaurants than ever before. Those premium dairy, produce, and protein costs add up quickly.

Based on what we now know about the changing restaurant cost landscape, let’s pretend for a moment.

Assume your menu prices don’t change, food costs increase by 3%, and your wages increase by 4%. You’ll start the year with a 6.2% profit margin and end the year with only a 3.8% profit margin. The price of inaction will set you on a quick path to the “good enough” trap.

In working with thousands of restaurant owners and operators across the industry, I’ve found that the most successful restaurateurs are constantly improving their business and finding opportunities to reduce costs and increase profits. These operators not only stay in business, but go on to open new and successful locations. Here are three best practices I’ve learned from them that can help you avoid falling into the “good enough” trap:

Schedule 15mins to chat with a product specialist

Start a FREE Trial Today! BevSpot offers full product education and account setup for all customers! No card Information needed!